From Credit Spreads to Broken Wing Butterflies

🛠️ Rebuilding the Framework After a Year of 10-Delta Spreads

After publishing Back to Structure a few days ago, I spent the next several days doing the technical work that had to come next: reviewing the mechanics of my old credit spread structures, going back to the original risk logic, studying alternative structures, modeling setups in OptionStrat, and rebuilding the execution process around a more mature framework.

The main conclusion was simple: the market idea behind 10 Delta Playbook still makes sense. Markets often reach zones of stretched momentum where continuation becomes less efficient, while option premium remains attractive enough to structure a defined-risk trade around that condition.

What needed to evolve was the structure.

A simple weekly credit spread does not always provide enough space when a strong move continues longer than expected.

That is why the next phase of 10 Delta Playbook will be built around a more mature options structure:

👉 Call Broken Wing Butterfly 👈

This framework is an evolution of the original credit spread logic — built around the same premium-selling philosophy: stretched movement, elevated RSI, rich premium, defined risk, and probability-based positioning.

What changes is the structure itself: more time, more asymmetry, and a more flexible risk geometry better suited for continuation-heavy market conditions.

Why 10-Delta Bear Call Spreads Worked for So Long

For almost a year, my weekly workflow revolved around 10-delta credit spread structures — primarily Bear Call Spreads, with occasional Put Credit Spreads built around the same probability-driven logic.

Over that period, I publicly documented 52 structured trades built around the same probability-driven framework: stretched upside movement, elevated RSI, rich premium, and defined-risk positioning through short-duration credit spreads.

The series remained highly consistent for a long time — until one sharp failure exposed how sensitive a narrow weekly structure can become when momentum expansion continues much further than expected.

Where a Simple Credit Spread Becomes Limiting

The core logic behind credit spreads still makes sense to me: sell premium around stretched conditions, define the risk upfront, and let probability and time work together.

The limitation appears in the structure itself:

A narrow weekly spread becomes increasingly sensitive when momentum continues expanding longer than expected. As expiration approaches, the trade compresses into a much more timing-dependent position, leaving very little flexibility if the original idea is correct but early.

That is ultimately what pushed me toward a structure that keeps the same premium-selling philosophy, but provides more space, more asymmetry, and a more adaptive payoff profile.

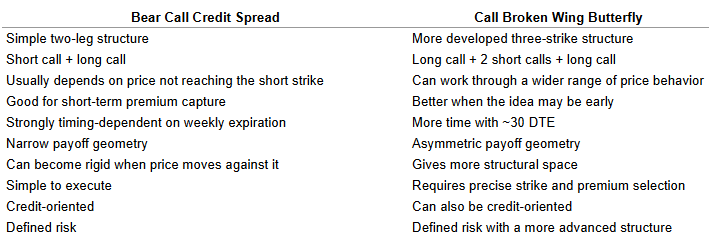

Credit Spread vs Broken Wing Butterfly

The idea finally crystallized after studying SMB Capital’s discussion:

What immediately stood out to me was that Broken Wing Butterfly was not some completely different philosophy. Structurally, it felt like a more advanced evolution of the same premium-selling logic I had already been trading through weekly credit spreads.

The important point: Broken Wing Butterfly does not replace the philosophy behind credit spreads. It extends it into a more flexible and structurally balanced framework.

This is the key comparison:

That is why I do not see BWB as a completely different strategy.

I see it as the next structural evolution of the same framework.

Why the Focus Is Now Around 30 DTE

Weekly trades were fast and efficient, but short expirations create heavy timing pressure. If momentum continues for several more sessions, a narrow weekly structure can become rigid very quickly as gamma exposure accelerates into expiration.

That is why the new framework shifts toward structures opened around ~30 DTE.

The purpose of the longer duration is not to hold positions into expiration, but to open trades with a more stable and flexible risk structure from the start.

In practice, most positions will still be managed actively and often closed much earlier — frequently within about a week — depending on how the price action develops.

The framework now prioritizes structurally balanced entries and active position management instead of expiration-dependent execution.

How the New Framework Works

Broken Wing Butterfly structures need liquidity. They need reliable option chains, tight bid/ask spreads, working greeks, and the ability to quickly check the full structure in OptionStrat.

That is why the current asset universe is limited to:

SPY, QQQ, IWM, AMD, AAPL, MSFT, TSLA, NVDA, AMZN, META, SLV, GLD, TLT, NFLX, GOOG, MU, PLTR.

The new selection logic works like this:

RSI and volatility rank are evaluated first.

Assets with elevated RSI and strong prior upside expansion become primary candidates.

Expiration is selected around ~30 DTE.

The short center call is selected around 20-delta.

The lower call wing is selected around roughly 70% of the short call premium.

The upper call wing is selected cheaper, roughly around 15% of the short call premium.

The structure must open for at least ~$100 net credit per 1-contract structure.

SAFE structures pass a max-loss filter of up to roughly ~$2,000.

HIGH_RISK structures may still appear if the minimum credit threshold remains attractive.

A Private Terminal for the New Phase

After a year of preparing trades manually, it became clear that the next version of the framework needed to be more than an idea. It needed to become a working tool.

That is why I built Options Strategist —

a private Telegram terminal for paid subscribers.

It is not a signal bot and it does not replace judgment with a button.

Its purpose is to automate structure preparation inside a clearly defined framework.

It handles the parts that take time manually and can easily break under pressure:

✅ filters liquid assets and option chains;

✅ prepares asymmetric Broken Wing Butterfly structures automatically;

✅ validates credit, risk, and structure quality;

✅ blocks unstable or incomplete market data;

✅ generates direct OptionStrat links with the full structure already built.

Paid subscribers get direct access to this workflow through Telegram authorization using the same email address tied to their subscription.

This is where preparation for new weekly structures will now begin.

What Changes Now in 10 Delta Playbook

The old weekly credit spread framework is now retired as the primary structure inside the project.

From this point forward, the focus shifts toward systematically built Call Broken Wing Butterfly positions executed through the new framework and workflow described above.

A new public trade log will continue to be maintained transparently, with real-money positions, real entries, real exits, and fully documented weekly execution.

Some weeks may produce one setup. Some weeks may produce several. But the process itself will remain systematic.

The goal now is not simply to find premium. — The goal is to continue refining a repeatable and structurally disciplined approach to options trading in public.

Thank you to everyone following the project so far.

More structures ahead.

Disclaimer

All content is for informational purposes only and does not constitute financial advice.Any trades or strategies should be tested in a simulated environment before use.Trading involves risk, and all decisions are the sole responsibility of the reader.